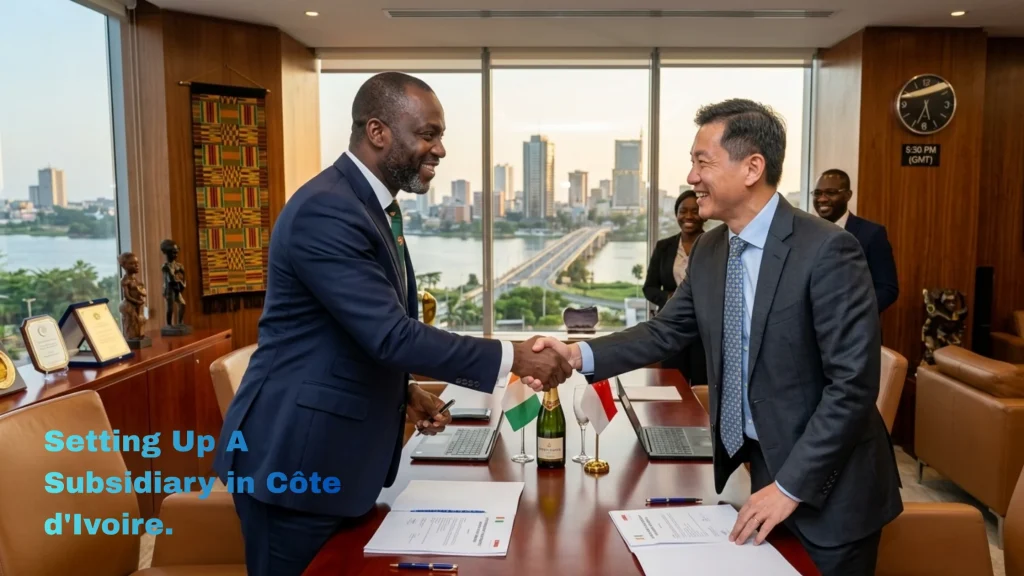

In the rapidly evolving economic landscape of West Africa, Ghana stands out as a beacon of opportunity. However, for both job seekers and employers, the biggest challenge has often been a lack of centralized, reliable data. Enter the Ghana Labour Market Information System (GLMIS), a digital revolution designed to bridge the gap between talent and opportunity.

Whether you are a graduate looking for your first break, an employer searching for the perfect hire, or an international firm looking to plant roots in Accra, understanding the GLMIS ecosystem is your first step toward success. In this guide, we’ll break down every facet of the GLMIS and explain why partnering with GroConsult Workforce Management Support is the secret weapon for any company looking to expand in the region.

What is the GLMIS? Understanding Ghana’s Digital Labour Hub

The Ghana Labour Market Information System (GLMIS) is more than just a job board; it is a sophisticated, data-driven platform managed by the Ministry of Employment and Labour Relations (MELR). Its primary goal is to provide a one-stop shop for everything related to the world of work in Ghana.

The Vision Behind GLMIS

The system was built to address “information asymmetry.” In the past, job seekers didn’t know where the jobs were, and employers couldn’t find qualified candidates. By centralizing data from the public and private sectors, the GLMIS provides:

Real-time labour statistics.

A centralized portal for job postings.

Information on Technical and Vocational Education and Training (TVET).

Career guidance resources.

1. The Job Seeker Portal: Transforming Careers

For the thousands of graduates entering the Ghanaian workforce every year, the GLMIS is a vital resource. It moves beyond the traditional “who you know” recruitment model to a “what you know” merit-based system.

Key Features for Candidates:

Profile Building: Users can create detailed professional profiles that serve as digital CVs.

Job Matching: The system uses algorithms to match a candidate’s skills with active job openings.

Resource Library: Access to templates for CV writing, interview tips, and cover letter guides.

Why Skill Alignment Matters

The GLMIS emphasizes “Skills for the Future.” By analyzing the data on the portal, job seekers can see which industries are growing, such as ICT, Agribusiness, and Renewable Energy, and tailor their training accordingly.

2. Empowering Employers: A Smarter Way to Hire

Hiring in a new market can be daunting. For Ghanaian businesses and multinational corporations alike, the GLMIS provides a structured environment to find vetted talent.

Streamlined Recruitment

Employers can post vacancies, filter through applications, and manage the hiring pipeline directly through the portal. This reduces the cost of recruitment and ensures that job advertisements reach a national audience.

Data-Driven Hiring

The GLMIS provides employers with insights into wage trends and labour availability in specific regions. For instance, if a company wants to open a factory in the Western Region, it can use GLMIS data to check the density of skilled technicians in that area.

3. The Role of TVET: Powering Ghana’s Industrialization

Technical and Vocational Education and Training (TVET) is a cornerstone of the GLMIS. The Ghanaian government has made a significant push toward “skilling up” the population to support the “Ghana Beyond Aid” agenda.

Connecting Training to Jobs

The GLMIS integrates information from various TVET institutions. This allows:

Students are to find accredited training providers.

Industry to influence curricula to ensure students are learning relevant skills.

Government to track the employment rate of vocational graduates.

4. Labour Market Statistics: The Pulse of the Nation

One of the most powerful aspects of the GLMIS is its role as a data repository. For policymakers and researchers, the system generates reports that define the economic trajectory of the country.

What Data is Tracked?

Unemployment Rates: Broken down by age, gender, and region.

Sectoral Growth: Identifying which industries are contributing most to the GDP.

Wage Benchmarks: Helping to establish fair compensation across different industries.

5. Strategic Expansion: Why GroConsult is Your Go-To Partner

While the GLMIS provides the data and the platform, navigating the cultural and regulatory nuances of the Ghanaian market requires a boots-on-the-ground partner. This is where GroConsult Workforce Management Supportexcels.

Positioning Your Business for Success

For any company looking to expand in Ghana or the wider West African region, GroConsult serves as the bridge between government data and corporate execution.

Why Choose GroConsult?

Local Expertise, Global Standards: GroConsult understands the local labor laws (Labour Act 651) and ensures that your expansion is fully compliant.

End-to-End Workforce Management: From payroll outsourcing to performance management, they handle the “people” side of your business so you can focus on growth.

Recruitment Mastery: While the platform provides a pool of candidates, GroConsult uses advanced headhunting techniques to find the top 1% of talent that fit your company culture.

Scaling with Confidence: Whether you are a startup or a Fortune 500 company, GroConsult’s bespoke HR solutions are designed to scale with your operations.

6. Career Guidance and Counselling: Shaping the Next Generation

The GLMIS isn’t just for those already in the workforce. It plays a crucial role in early career intervention.

The portal offers tools for secondary and tertiary students to explore career paths. By understanding the “In-Demand” skills listed on the portal, students can make informed decisions about their majors, reducing the rate of graduate underemployment.

7. The Legal Framework: Labour Laws and GLMIS

Operating within the GLMIS ecosystem means adhering to Ghana’s strict but fair labour regulations. The system helps promote:

Fair Wages: Ensuring workers are not exploited.

Workplace Safety: Providing resources on health and safety standards.

Dispute Resolution: Information on how to handle grievances through the National Labour Commission.

Register with a valid email and National ID (GhanaCard).

Upload your certificates and build your profile.

For Employers:

Navigate to the “Employer” section.

Register your business using your TIN (Tax Identification Number).

Post your first vacancy and start receiving applications.

Conclusion: Your Gateway to Growth

The Ghana Labour Market Information System (GLMIS) is a powerful tool that brings transparency, efficiency, and data-driven decision-making to the forefront of the Ghanaian economy. By leveraging this platform, job seekers can find meaningful work, and employers can build world-class teams.

However, data is only half the battle. To truly thrive and scale in the region, you need a partner who understands the heartbeat of the local market.

Ready to expand your business in Ghana? Don’t navigate the complexities of workforce management alone. Let the experts guide you.

Yes, it is a public service provided by the Government of Ghana and is free for both job seekers and employers.

Q2: Do I need a GhanaCard to register?

Yes, for security and verification purposes, the Ghana card is the primary form of identification required for the portal.

Q3: Can foreign companies use GLMIS to hire?

Absolutely. However, for a more seamless experience and to ensure compliance with local content laws, it is recommended to work with a local partner like GroConsult.

Q4: What is the difference between GLMIS and private job boards?

GLMIS is the official government database. While private boards are great for listings, GLMIS is used for national statistics, policy planning, and access to government-backed training programs.

Q5: How can GroConsult help my business expand in Ghana?

GroConsult provides comprehensive workforce management, including recruitment, payroll, legal compliance, and HR strategy, acting as your local HR department.

The West African macroeconomic landscape is experiencing a subtle yet profoundly significant structural realignment, rendering the deployment of an Employer of Record (EOR) in Liberia an essential mechanism for international organizations targeting cross-border corporate expansion.

Historically recognized for its vast maritime registry and foundational extractive industries like iron ore, rubber, and gold, the Liberia of 2026 has successfully diversified its commercial narrative. Today, the nation is steadily cultivating a highly resilient, digitally literate, and natively English-speaking professional workforce, largely concentrated within metropolitan hubs like Monrovia, Paynesville, and Buchanan.

For expanding global enterprises and agile regional organizations, this creates an exceptional corporate opportunity. However, entering this unique marketplace introduces a classic operational dilemma. While the local talent ecosystem is wealthier and more eager to engage with international frameworks than ever before, the statutory architecture required to hire, manage, and compensate these professionals remains intensely strict.

The pressing challenge for foreign HR departments is no longer simply identifying top-tier operational leads or technical managers; it is understanding how to legally onboard and pay a distributed team without falling victim to severe compliance penalties, tax liabilities, or catastrophic labor disputes under the vigilant oversight of the Ministry of Labour and the Liberia Revenue Authority (LRA).

1. Why Using an Employer of Record (EOR) in Liberia is Now a Compliance Mandate

To resolve these administrative hurdles, partnering with an enterprise-grade Employer of Record (EOR) in Liberia has transitioned from a structural alternative into an absolute compliance mandate. When an international organization decides to establish an operational footprint in Liberia, it is immediately confronted by a highly protective, post-reform statutory environment defined by the comprehensive Decent Work Act of 2015, complex multi-tiered social security frameworks, and a uniquely nuanced dual-currency economic system where the United States Dollar (USD) and the Liberian Dollar (LRD) circulate interchangeably.

Attempting to build a localized human resources division from scratch before validating your long-term product-market fit can deplete corporate capital and delay operational rollouts by several months. By leveraging a professional local EOR partner, your business can entirely bypass the heavy bureaucratic friction of direct legal entity incorporation. Instead, you utilize a pre-existing, fully compliant institutional vehicle to employ the exact professional teams you need to drive your primary commercial objectives.

This comprehensive strategic blueprint details the foundational regulatory mechanisms of the Liberian labor market in 2026, offering actionable compliance insights for forward-thinking companies looking to master workforce management in West Africa.

2. Macroeconomic Trajectories: The Strategic Context for an Employer of Record (EOR) in Liberia

To fully appreciate the scope of corporate opportunity unfolding across Liberia, one must analyze the intentional coordination between current public policy and private sector formalization. The 2026 Liberian economy is characterized by a steady real GDP growth rate projecting around 4% to 5% annually, operating alongside a structured national digitization agenda spearheaded by the Liberia Revenue Authority.

A key regulatory driver shaping this environment is the state’s aggressive enforcement of worker safety and occupational standards, highlighted by the Ministry of Labour’s recent official implementation of Regulation No. 19 on Occupational Health, Safety, and Welfare in the Workplace, in strict alignment with Chapter 29.3 of the national labor laws.

This means that foreign companies entering the Liberian marketplace are entering an environment where employee protections are heavily scrutinized, and the old paradigms of informal hiring are being rapidly replaced by institutional transparency.

Liberian Macroeconomic Foundation (2026)

Real GDP Growth: ~4% – 5% Per Annum

Official Language: English (Native Corporate Fluency)

Primary Currency Landscape: Dual-Currency System (USD & LRD)

Statutory Oversight: Ministry of Labour & Liberia Revenue Authority (LRA)

Furthermore, Liberia holds a distinct structural advantage over many of its regional neighbors for North American and European enterprises: English is the official national language. This eliminates the extensive translation overhead and cultural friction frequently encountered across Francophone or Lusophone Africa, enabling local hires to integrate seamlessly into global technical, administrative, and creative frameworks from their very first day on the job.

However, capturing the full operational advantages of this talent surge requires absolute alignment with local wage standards. While the historical statutory minimum wage remains set at 15 LRD per hour for unskilled laborers (roughly equivalent to $0.68 per hour or $5.50 per day) and $3.50 per day for domestic workers, the competitive market rate for skilled professionals in fields like finance, logistics, tech, and NGO management sits significantly higher, frequently benchmarked between 35,000 LRD and 40,000 LRD per month as a baseline for junior staff.

Navigating this wage landscape while staying fully aligned with the strict reporting mandates of the Ministry of Labour requires deep local expertise—a capability that a professional Employer of Record (EOR) in Liberia automatically embeds into your expansion strategy.

3. Deconstructing the Liberia Decent Work Act: Managing Contracts with an Employer of Record (EOR) in Liberia

The legal foundation of any successful workforce management strategy in Monrovia or beyond is an absolute, uncompromised mastery of the Liberia Decent Work Act of 2015. Under the clear terms of this legislation, employment agreements must be highly formalized, with a strong statutory preference for explicit, written employment contracts. The law strictly delineates between Fixed-Term Contracts designed for specific, time-limited projects, and Indefinite Contracts that govern permanent corporate roles.

A critical operational nuance that frequently blindsides foreign HR departments is that any employment contract must clearly specify the core parameters of the role, the precise calculation of wages, and the specific currency of remuneration. Under Chapter 2 of the Act, if an employer fails to deliver a comprehensive written statement of these terms within the initial weeks of employment, the worker is granted substantial legal leverage in the event of a contractual dispute before the Labor Commissioner.

Managing probationary periods under the Liberian framework requires precise chronological planning, as the Decent Work Act establishes clear boundaries to protect newly hired staff from extended exploitation under temporary terms. Under statutory caps, the maximum allowable length of a standard corporate probationary period is strictly limited to three months. This trial window is designed to give both the employer and the employee an opportunity to evaluate operational fit under simplified separation guidelines.

During this three-month window, either party can dissolve the employment relationship by providing a brief, written notice of termination—typically seven days—without triggering the extensive severance liabilities or complex redundancy justifications required for permanent staff.

However, an enterprise must actively monitor this timeline: if the three-month probationary window expires and the employee continues to perform tasks, log hours, or receive compensation without a formal written extension or termination notice, the law deems the employment relationship to be automatically confirmed as a permanent, indefinite contract. Once this invisible threshold is crossed, the worker instantly inherits full statutory job security, making any future separation an intensely regulated legal process.

Contractual Notice and Tenure Framework

Contractual Phase

Maximum Statutory Duration

Mandatory Written Notice Windows

Probationary Period

3 Months

7 Days’ written notice required for separation

Short-Term Tenure

3 to 6 Months

2 Weeks’ written notice required for separation

Mid-Term Tenure

6 to 12 Months

3 Weeks’ written notice required for separation

Confirmed Permanent Status

1+ Years of Service

4 Weeks’ written notice required for separation

4. Working Hours, Overtime Tiers, and Rest Periods

Once your local Liberian team is successfully onboarded, daily operations must adapt to the statutory constraints governing working hours and weekly rest mandates. Under Section 17.1 of the Decent Work Act, the standard maximum ordinary working hours for the formal commercial sector are set at 8 hours per day and up to 48 hours per week, typically distributed across a six-day framework, though standard corporate environments and technology firms frequently self-regulate to a 40-hour, five-day workweek from Monday through Friday.

The law also establishes a rigid safety constraint under Section 17.5: the absolute maximum daily duration of work, including any requested or voluntary overtime hours, can never exceed 12 hours in a single calendar day, and every worker must be granted an uninterrupted 24-hour rest period during each seven-day operational cycle.

Any professional activity demanded of an employee beyond their standard ordinary daily or weekly limit is legally classified as overtime, requiring precise, tiered financial premiums to be calculated and distinctly displayed on the employee’s monthly payslip to satisfy the rigorous verification procedures of visiting labor inspectors.

Statutory Overtime Multipliers:

Standard Working / Rest Days: 150% of the regular hourly rate (1.5x pay).

Official Public Holidays: 200% of the regular hourly rate (2.0x double pay).

Manually tracking these hours across a distributed team of remote consultants or local field technicians can quickly overwhelm an overseas payroll department. An experienced provider of Employer of Record (EOR) in Liberia eliminates this risk by deploying automated, fully localized time-tracking software that natively integrates with Liberian statutory premium structures.

Important Compliance Note: While autonomous high-level executives and managing directors can be contractually excluded from hourly overtime tracking by explicitly structuring their contracts with an inclusive, all-in global executive compensation package, standard clerical staff, technical support teams, and field workers must have their overtime hours tracked and remunerated precisely as mandated by Section 17 of the Decent Work Act.

5. Payroll Architecture: Tax, NASSCORP, and LRA PAYE Management

Executing compliant payroll operations within Liberia requires an intricate understanding of a multi-layered tax and social contribution matrix, operating within a unique dual-currency ecosystem. Employers face serious statutory liabilities administered by the National Social Security and Welfare Corporation (NASSCORP). Under the updated national insurance frameworks, the total employer-funded social security burden is optimized across foundational retirement and injury funds.

On the employee side, the worker is responsible for a statutory deduction from their gross salary to co-fund their retirement asset base, which the employer is legally mandated to withhold at source and remit alongside the employer portion to NASSCORP by the final day of the payment month.

Financial Breakdown of a Compliant Liberian Gross Salary

Gross Salary (USD / LRD Allocation) Employer Social Liabilities (NASSCORP): Contribution allocated to the National Pension Scheme and the Employment Injury Scheme.

Employee Statutory Deductions: NASSCORP Employee Retirement Contribution. LRA PAYE Income Tax: Calculated based on a progressive annual scale (0% up to top marginal bands).

In addition to social security accounting, the employer must act as an active withholding agent for the PAYE (Pay As You Earn) income tax system, which is strictly regulated by the Liberia Revenue Authority. For resident individuals, personal income tax is calculated using a progressive annual scale built across distinct tax bands, operating with a tax-free baseline.

For earnings above this threshold, the brackets scale progressively, topping out at a maximum marginal rate for high-income earners. For non-resident individuals performing remote services within the territory, the LRA demands a flat 20% withholding tax on all Liberian-sourced employment income, entirely stripping away standard brackets or deductions.

Furthermore, because corporate operations are frequently funded in USD while local statutory reporting must often be recorded or balanced against LRD conversions, managing a compliant dual-currency payroll introduces a layer of volatile exchange-rate risk and complex reconciliation. A professional Employer of Record (EOR) in Liberia completely absorbs this operational burden, running accurate dual-currency calculations, insulating your parent firm from exchange errors, and guaranteeing that all tax withholdings are successfully remitted to the LRA by the mandatory monthly deadlines.

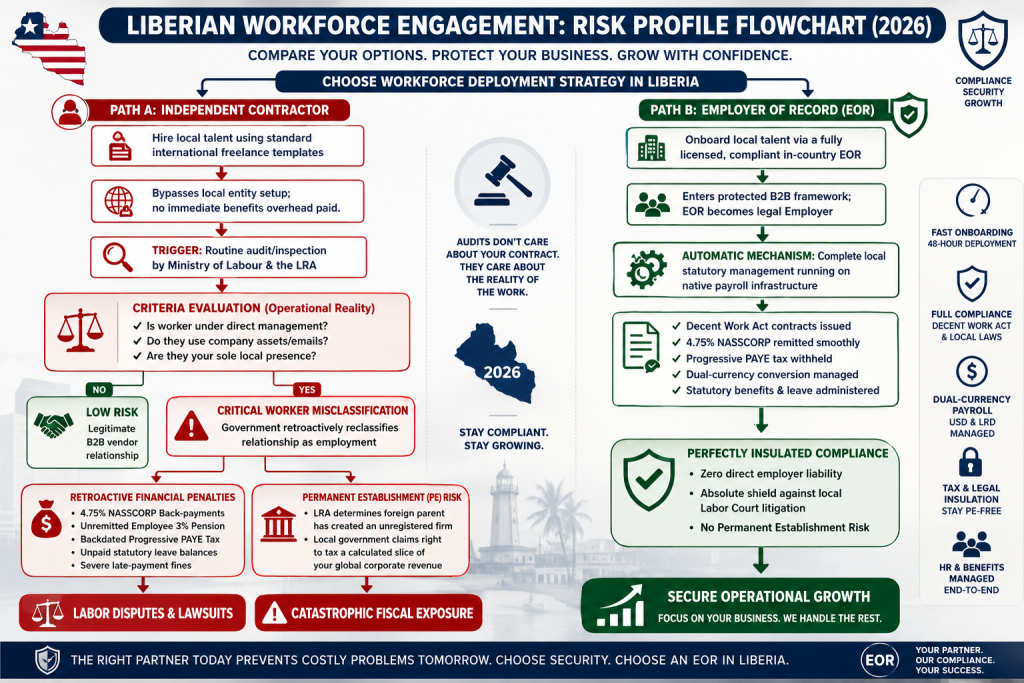

6. Worker Misclassification and Permanent Establishment Defenses

For international technology firms, global consultancies, and expanding commercial enterprises, the single greatest legal and financial threat when entering the Liberian market stems from the misclassification of local talent as independent contractors. To bypass local payroll setups, minimize benefits overhead, or quickly test market dynamics, many foreign companies choose to engage Liberian software engineers, project managers, or business development agents through standard international freelance templates or remote service agreements.

In 2026, this approach represents an exceptionally high-risk compliance gamble. Both the Ministry of Labour and the Liberia Revenue Authority have radically increased their field audit and digital tracking programs, specifically targeting foreign enterprises utilizing localized “consultants” who behave, in reality, as standard corporate employees.

Under the regulatory definitions enforced in Liberia, if a local professional provides services exclusively for your foreign organization, operates under your direct managerial control, relies on company-provided assets, or represents your business using an official corporate identity, local authorities will legally reclassify the relationship as a disguised employment contract.

The penalties for worker misclassification in Liberia are severe: your organization can be held retroactively liable for years of unremitted NASSCORP employer social contributions, the employee’s unwithheld retirement allocation, unpaid progressive PAYE taxes, mandatory annual leave back-pay, and steep late-payment fines.

Even more dangerously, if that independent contractor is found to be continuously negotiating client agreements or executing core corporate strategies on your behalf within the territory, the LRA can rule that your international enterprise has established a Permanent Establishment (PE) in Liberia. This legal determination grants the local government the authority to retroactively assess corporate income tax against a calculated portion of your global corporate revenue.

Utilizing a professional Employer of Record (EOR) in Liberia completely eliminates these existential threats. By legally employing the talent through a fully registered, compliant in-country entity and leasing them back to you under a protected B2B service framework, the EOR forms an absolute compliance shield, ensuring your company remains perfectly insulated from direct corporate tax and labor court liabilities.

7. Leave Allocations, Maternal Protections, and Legal Offboarding Frameworks

Building a high-performance, sustainable corporate culture in Liberia requires a deep, systematic commitment to the employee wellness and leave mandates embedded within national statutes. The Decent Work Act grants full-time workers highly structured paid annual leave benefits that must be carefully managed by HR departments.

Upon completing one full year of continuous service with an employer, an individual is legally entitled to paid annual leave based on their tenure, which scales progressively to ensure that long-term loyalty is contractually rewarded. Employers are strictly required by law to pay the employee’s standard base wages for their annual leave period completely in advance before the vacation begins, ensuring the worker has full financial access to their rest period.

Beyond standard annual vacation, the Liberian framework provides expansive protections for family milestones and medical emergencies, reflecting the deep socio-cultural values of West Africa. Female professionals are entitled to a minimum of 14 weeks of fully paid maternity leave, a framework designed to secure strong job security and health protections around childbirth. This leave is covered at 100% of their standard regular pay rate, and the law strictly prohibits employers from executing any termination notice or structural role modification while a female worker is out on maternity leave. Employees are also eligible for paid sick leave allocations upon presentation of a valid medical certificate issued by a registered practitioner.

Short-Term Service (3 – 6 Months): 2 Weeks’ Written Notice Required

Mid-Term Service (6 – 12 Months): 3 Weeks’ Written Notice Required

Long-Term Service (1+ Years): 4 Weeks’ Written Notice / Severance Eligible

When an employment relationship must come to an end, navigating the offboarding phase under Liberian law requires strict adherence to the statutory notice periods outlined in the Decent Work Act to avoid costly wrongful termination lawsuits before the Labor Commissioner. Except in cases of proven gross misconduct (faute lourde), terminating a contract requires the employer to issue a formal written notice based on length of service.

Furthermore, if a termination is executed due to economic redundancy or structural downsizing, the employer is legally obligated to pay a comprehensive statutory severance package calculated against the employee’s tenure and historical salary metrics. A local EOR partner ensures that every step of this delicate offboarding lifecycle—from initial notice delivery to the final calculation of the final settlement (solde de tout compte)—is executed flawlessly, protecting your corporate reputation and preventing damaging litigation.

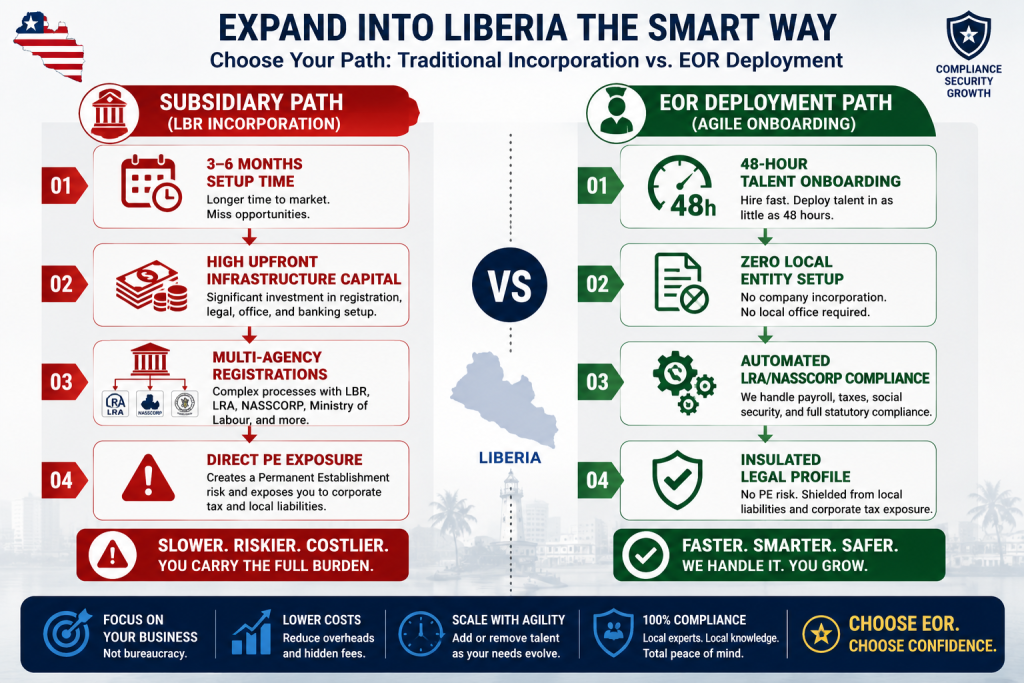

8. Strategic Agility: Traditional Local Incorporation vs. An Employer of Record (EOR) in Liberia

For corporate leadership evaluating expansion paths into West Africa, the ultimate operational choice boils down to a fundamental comparison: Is it wiser to incorporate a standalone local subsidiary, or should your organization leverage the immediate agility of an in-country Employer of Record (EOR) in Liberia?

Establishing a traditional legal entity in Liberia through the Liberia Business Registry (LBR) is a lengthy, bureaucratic, and capital-intensive endeavor. The process requires substantial upfront capital injection, extensive notarization of corporate bylaws, physical registration across separate tax and social security databases, the complex opening of localized commercial corporate bank accounts, and the continuous retention of local legal counsel to manage ongoing monthly tax filings. This administrative setup path routinely takes anywhere from three to six months to become fully operational, leaving your expansion plans vulnerable to changing market dynamics and regional competitors who move with greater speed.

Conversely, utilizing an established, fully licensed provider of an Employer of Record (EOR) in Liberia completely transforms your market entry timeline. Because the EOR provider already owns a pristine, fully compliant corporate entity in Monrovia, the entire onboarding and local hiring process can be finalized in as little as a few business days.

The EOR partner assumes 100% of the legal employer responsibilities, taking charge of compliant contract drafting under the Decent Work Act, processing dual-currency monthly payroll, managing NASSCORP and LRA PAYE remittances, tracking complex holiday overtime tiers, and handling statutory benefits administration.

This rapid deployment model dramatically lowers your upfront infrastructure overhead, allowing your executive leadership to focus entirely on product localization, market acquisition, and operational growth. If your organization ever decides to pivot or scale back its regional operations, an EOR framework allows you to gracefully exit the market within standard statutory notice periods, completely unburdened by the years-long, highly bureaucratic process of legal entity liquidation.

Empowering Your Global Growth Safely

The dynamic commercial ecosystem of Liberia in 2026 offers an unparalleled horizon of opportunity for forward-thinking enterprises ready to harness the historic human capital surge flowing through West Africa. Yet, as the Liberian government aggressively formalizes its economy and intensifies labor compliance enforcement under strict new workplace safety and tax verification regulations, the margin for administrative error has effectively dropped to zero.

Managing an international workforce across borders is no longer a challenge that can be handled via remote HR templates or informal independent contractor workarounds. To truly thrive in the Liberian marketplace, your organization requires a sophisticated, highly compliant localized foundation.

By partnering with an elite in-country partner, you effectively bridge the gap between global strategic ambition and localized legal reality. An EOR allows your organization to secure the absolute best minds in Monrovia, maintain flawless compliance with the complex Decent Work Act, insulate your core business from permanent establishment risks, and optimize your entire workforce management lifecycle under a single, highly efficient framework.

Leave your thoughts, challenges, or expansion questions in the comments section below, or reach out to our dedicated teams today to schedule a comprehensive compliance audit for your organization.

Frequently Asked Questions (FAQs)

What is an Employer of Record (EOR) and how does it function in Liberia?

An EOR is a professional services firm that acts as the legal employer of your workers within Liberia. While you maintain direct day-to-day operational control over the employee’s deliverables, the EOR provider absorbs all statutory liabilities, including onboarding, drafting contracts compliant with the Decent Work Act, running monthly payroll, and handling tax and social security filings.

What is the statutory minimum wage floor in Liberia for 2026?

Under current regulations, the historical minimum wage floor remains set at 15 LRD per hour for unskilled formal laborers (approximately $0.68 per hour or $5.50 per day) and $3.50 per day for domestic staff. However, skilled professionals in corporate sectors command significantly higher competitive market salaries, usually ranging from 35,000 LRD to 40,000 LRD per month as a minimum baseline.

How are NASSCORP social security contributions managed by an Employer of Record (EOR) in Liberia?

The National Social Security and Welfare Corporation (NASSCORP) mandates strict tracking of gross earnings. An EOR managed payroll calculates and deducts the appropriate employee contributions at source while funding the mandatory employer allocations for the national pension and employment injury schemes, remitting the totals directly to NASSCORP before monthly deadlines.

Can an international company pay its Liberian employees in US Dollars (USD)?

Yes. Liberia operates a distinct dual-currency economic system where both the United States Dollar (USD) and the Liberian Dollar (LRD) are recognized as legal tender. An EOR provider ensures that payroll is compliant with local currency tracking, managing the complex exchange-rate conversions required for LRA tax reporting.

What are the maximum probationary timelines allowed under the Liberia Decent Work Act?

Under the Decent Work Act of 2015, the maximum allowable duration for a standard corporate probationary period is strictly capped at three months. If an employee continues working past this three-month threshold without receiving a written termination or formal extension notice, their contract automatically converts to a permanent, indefinite contract status.

Utilizing comprehensive Employer of Record (EOR) Solution in Ghana has become the primary mechanism for international firms to shield themselves from devastating financial audits, employment lawsuits, and structural operational liabilities in West Africa. Imagine a scenario that is playing out with increasing frequency across the corporate boardrooms of multinational organizations: Your expanding enterprise has just identified a stellar talent cohort of software engineers, cloud architects, and operations managers located in Accra, Ghana.

Their language fluency is pristine, their technical portfolios rival those found in Silicon Valley or London, and their baseline compensation profiles align perfectly with your global engineering budget. To move with speed, your HR department bypasses traditional local entity incorporation and quickly onboards these specialists using international independent contractor templates.

For the first nine months, your West African operations are a ringing success. Deliverables cross the digital pipeline ahead of schedule, and regional market penetration accelerates. Then, a formal notification from the Ghana Revenue Authority (GRA) arrives at your global headquarters.

Following a targeted cross-agency digital audit of local banking transactions and operational emails, the state has legally reclassified your “independent contractors” as full-time, regularized employees. Suddenly, your firm is facing immediate, retroactive demands for unremitted Pay-As-You-Earn (PAYE) taxes matching Ghana’s top 35% marginal tax bracket, compounded by severe late-payment penalties. Simultaneously, the Social Security and National Insurance Trust (SSNIT) initiates legal proceedings for unremitted pension obligations under the newly upgraded 2026 statutory limits. Within forty-eight hours, an agile market entry strategy transforms into a catastrophic compliance crisis.

For international brands eyeing the sub-Saharan marketplace, the primary challenge of workforce scaling is no longer about finding premium talent—it is about establishing a flawless compliance infrastructure. To navigate these rising regulatory tides, partnering with an established provider of Employer of Record (EOR) Solution in Ghana has transformed from a structural alternative into an absolute corporate risk management mandate.

This comprehensive corporate guide details how expanding organizations can leverage an enterprise-grade Employer of Record (EOR) Solution in Ghana to entirely eliminate systemic employment, tax, and legal risks within the Ghanaian territory.

1. The 2026 Macroeconomic Realities Demanding Employer of Record (EOR) Solution in Ghana

To successfully operate in the modern Ghanaian commercial ecosystem, cross-border corporate leadership must look past historical market paradigms. The contemporary business landscape in Ghana is defined by an aggressive, data-driven push toward digital tax tracking and formal economic integration. The Ghana Revenue Authority has successfully overhauled its operational enforcement capabilities, deploying integrated e-reporting platforms and predictive data-matching algorithms that analyze corporate bank accounts and individual tax filings in real time.

Concurrently, the National Tripartite Committee (NTC) officially increased the National Daily Minimum Wage to GH¢ 21.77 per day (effective January 1, 2026), representing a 9% year-over-year adjustment from previous limits. This structural change establishes a non-negotiable statutory floor for all employers operating within the jurisdiction. For international enterprises, this data-driven economic climate provides excellent operational transparency but demands absolute, uncompromised alignment with localized reporting tools from day one.

Ghanaian Commercial Baseline (2026)

├── National Daily Minimum Wage: GH¢ 21.77 per day

├── Target Remittance Filing Deadline: 15th of every subsequent month

├── Top Marginal Income Tax Bracket: 35% for income exceeding GH¢ 50,000/month

└── Statutory Oversight Agencies: GRA, SSNIT, and the National Labour Commission (NLC)

At the same time, the Ministry of Employment and Labour Relations has significantly expanded its physical field inspection initiatives. Traveling task forces regularly audit corporate workspaces in urban commerce hubs like Accra, Kumasi, and Takoradi to ensure foreign entities are not exploiting the informal labor sector. Attempting to manage local remote personnel through a remote global HR department without native administrative infrastructure exposes your brand to sudden stop-work orders and public reputational damage.

By deploying specialized Employer of Record (EOR) Solution in Ghana, your organization establishes an immediate, fully localized compliance buffer. The EOR provider integrates your daily personnel workflows with the GRA’s official electronic pipelines, securing your regional presence while insulating your primary corporate structure from direct regulatory friction.

2. Deconstructing the Ghana Labour Act with Employer of Record (EOR) Solution in Ghana: Contract Vulnerabilities and Probation Traps

The legal foundation of any sustainable workforce management strategy in West Africa is a comprehensive understanding of the Ghana Labour Act, 2003 (Act 651). Under Section 12 of Act 651, any employment agreement extending beyond a continuous duration of six months must be formalized as a comprehensive written contract. This document must explicitly outline the worker’s operational title, job descriptions, date of initial appointment, detailed wage rates, structured payment intervals, standard weekly hours, vacation allocations, and conditions relating to medical incapacity.

The law strictly differentiates between Fixed-Term Contracts (designed for project-focused, time-bound deliverables) and Indefinite-Term Contracts for permanent corporate positions. A common and highly costly corporate risk involves failing to define explicit contract parameters, which often prompts the National Labour Commission (NLC) to reclassify temporary teams as permanent staff, automatically granting them extensive separation protections and shifting long-term financial liabilities directly onto your balance sheet.

Managing probationary windows within the Ghanaian framework requires careful contract drafting and chronological accuracy. Unlike alternative regional jurisdictions that apply rigid statutory caps, Act 651 refers broadly to a “reasonable duration determined in advance”, leaving the exact trial window to be explicitly documented within the core employment agreement or applicable collective bargaining agreements (CBAs).

In standard corporate engineering and financial services workflows, this trial window is typically set between three to six months. During this probationary timeframe, the employment relationship can be severed by either party respecting a compressed notice window—statutorily established at one week (seven days) or payment in lieu of notice—without needing to go through complex redundancy justifications or severance payouts.

However, organizations must actively monitor these calendar timelines. If a probationary window expires and the employee continues to perform corporate tasks, log operational hours, or receive base compensation without a formal written extension or evaluation notice, the law deems the employee’s status as automatically confirmed.

Once this threshold is crossed, the worker instantly inherits full statutory job security and comprehensive termination notice protections, making any future separation a highly regulated, high-liability legal process. Professional Employer of Record (EOR) Solution in Ghana manage this delicate timeline automatically. EOR systems use localized HR software to track probationary dates, alerting global management teams well in advance and executing fully compliant contractual adjustments before hidden liabilities can form.

Employment Phase

Statutory Notice Timelines

Core Structural Risk Managed

Probationary Window (3–6 Mos)

7 Days’ Written Notice Required

Early-stage skill and culture alignment without long-term separation liabilities.

Short-Term Tenure (<3 Years)

2 Weeks’ Written Notice Required

Mitigates wrongful termination claims during mid-level structural realignments.

Long-Term Permanent Tenure

1 Month Minimum Written Notice

Prevents costly legal disputes before the National Labour Commission (NLC).

3. Standardizing Time Tracking and Overtime Compliance via Employer of Record (EOR) Solution in Ghana

Once a local Ghanaian team is successfully integrated into your global operations, daily shift schedules must adapt to the rigid statutory limits governing working hours and mandatory rest periods. Under the strict terms of the Ghana Labour Act, the standard legal workweek is fixed at 40 hours, typically managed as eight hours per day across a standard five-day sequence from Monday through Friday.

Any professional activity required of a worker beyond this 40-hour weekly threshold is legally classified as overtime. These extra hours require precise financial tracking and must be clearly broken down on the worker’s monthly payslip to satisfy the requirements of visiting labor inspectors.

The calculation of overtime premiums in Ghana must align with standard statutory benchmarks and company policies. Typically, standard overtime executed on regular business days is calculated at a premium rate of 1.5 times the standard hourly wage.

If your operational demands require employees to execute deliverables on weekends, official public holidays, or during designated night shifts, the financial requirements scale up significantly, often moving to 2.0 times the standard hourly wage. Manually tracking these hours across a distributed team can be incredibly challenging for a remote HR department.

Standard Hourly Base Rate

├── Regular Business Day Overtime: Base × 1.5 Premium Rate

└── Weekend & Public Holiday Overtime: Base × 2.0 Premium Rate

Expert Risk Management Note: While senior executives, managing directors, and autonomous technical leads can be contractually excluded from daily overtime tracking by integrating an all-inclusive gross salary model, standard administrative assistants, customer support agents, and operational staff must have their extra hours tracked and remunerated precisely as dictated by the law.

Failing to properly document and pay these premium tiers creates an immediate legal vulnerability. Disgruntled former employees can flag these gaps to initiate retroactive compensation claims before the National Labour Commission. Leveraging premium Employer of Record (EOR) Solution in Ghana entirely removes this vulnerability. The EOR partner deploys fully localized time-tracking software that logs every hour against the corresponding statutory premium tier, generating audit-ready payroll reports that protect your organization from wage disputes.

4. Mastering the 2026 GRA Tax Tiers and SSNIT Contribution Caps via Employer of Record (EOR) Solution in Ghana

Executing compliant payroll operations within the Ghanaian market requires an accurate understanding of the dual financial obligations comprising employer social contributions and individual income tax withholdings. Employers operating within the country face significant statutory liabilities administered by the Social Security and National Insurance Trust (SSNIT) under the National Pensions Act, 2008 (Act 766).

The employer-funded social security obligation is set at a flat 13% of the employee’s basic salary. Conversely, the employee contributes a flat 5.5% deduction from their basic salary, which the employer must withhold at source. This combines for a total mandatory contribution of 18.5%, which is split between the Tier 1 First-Tier scheme managed by SSNIT (13.5%) and the Tier 2 Mandatory Occupational Pension scheme managed by approved private trustees (5%).

A critical structural change taking effect is the significant upward adjustment of the maximum insurable earnings cap. The Social Security and National Insurance Trust, in direct consultation with the National Pensions Regulatory Authority (NPRA), officially raised the maximum insurable earning ceiling from GH¢ 61,000.00 to GH¢ 69,000.00 per month.

This structural cap increase significantly impacts operational budgeting for multinational firms employing high-earning local executives, senior engineers, and误expatriate staff. The maximum monthly Tier 1 contribution now reaches GH¢ 9,315.00. While the increased contribution up to the new GH¢ 69,000.00 cap qualifies for a corresponding tax relief against Pay-As-You-Earn calculations (softening the net income impact for high earners), the employer’s absolute wage bill automatically increases for any professional whose salary hits this ceiling.

In addition to pension assets, the employer must act as a withholding agent for the PAYE (Pay As You Earn) income tax system, which is administered by the Ghana Revenue Authority (GRA). The progressive monthly tax bands for individual resident taxpayers follow a graduated scale designed to tax higher earners progressively:

First GH¢ 490: 0% (Tax-Free Baseline)

Next GH¢ 110: 5%

Next GH¢ 130: 10%

Next GH¢ 3,000: 17.5%

Next GH¢ 16,395: 25%

Next GH¢ 29,875: 30%

Exceeding GH¢ 50,000 per month: 35% (Top Marginal Tax Bracket)

For non-resident individuals performing remote services within Ghana, the GRA applies a flat 25% withholding tax on all Ghana-sourced employment income, with no graduated bands or standard deductions permitted unless modified by an active Double Taxation Treaty (DTT).

These monthly payroll tax deductions and SSNIT contributions must be declared and remitted to the respective portals by the 15th day of the following month. Any delayed or inaccurate filing triggers immediate automated fines, compounding interest penalties, and heightened audit risks, all of which an EOR partner removes from your operational scope by managing the entire process on its own local balance sheet.

5. Mitigating Worker Misclassification and Permanent Establishment Traps Using Employer of Record (EOR) Solution in Ghana

For international firms exploring business opportunities in West Africa, the single most dangerous compliance vulnerability centers on worker misclassification and the downstream risk of Permanent Establishment (PE). To lower costs or skip administrative setups, many companies engage Ghanaian developers, sales executives, or localized consultants using standard international freelance agreements or independent contractor templates. This approach is highly risky. The Ghana Revenue Authority (GRA) and the Labor Department coordinate closely to look for hidden employment relationships to prevent tax evasion and protect the national labor market.

Independent Contractor Model (High Risk)

├── 100% Personal Exposure to Retroactive GRA Audits

├── Direct Risk of Permanent Establishment Corporate Taxation

└── Zero Local Pension (SSNIT) Protections

VSEmployer of Record (EOR) Solution in GhanaFramework (Insulated Risk)

├── Fully Compliant GRA Electronic Submission

├── Absolute Statutory SSNIT Remittance Under Local Legal Entity

└── Global Parent Corporation 100% Shielded from Local Corporate Tax

If a local contractor works exclusively for your international firm, reports to your corporate managers, relies on company-provided assets, or represents your business using an official corporate identity, the Ghanaian authorities will legally reclassify the relationship as a disguised employment contract. This reclassification forces the foreign enterprise to retroactively pay years of unremitted 13% SSNIT employer pension allocations, the employee’s unwithheld 5.5% contribution, unpaid progressive PAYE taxes, mandatory annual leave back-pay, and steep late-payment fines.

Even more dangerously, if that independent contractor is found to be continuously negotiating local contracts or executing corporate strategies on your behalf, the GRA can declare that your business has formed a Permanent Establishment in Ghana. This allows local authorities to assess corporate income tax against a portion of your global corporate revenue.

Utilizing a professional local Employer of Record (EOR) Solution in Ghana provider completely eliminates this operational risk. By hiring your local talent directly through our fully compliant in-country legal entity and leasing them back to you, we establish a robust legal barrier, ensuring your business stays fully aligned with both the GRA and the Ghana Labour Act.

6. Managing Statutory Leave Protections and Offboarding Protocols with Employer of Record (EOR) Solution in Ghana

Creating an engaging, high-retention corporate culture in Ghana requires a thorough commitment to the employee wellness benefits mandated by local statutes. Under Section 20 of the Labour Act, every full-time worker is entitled to a minimum of 15 working days of fully paid annual leave after completing one full year of continuous service. The law dictates that any agreement to safeguard or relinquish the entitlement to paid annual leave is completely void, meaning workers must physically take their leave, and untaken leave must be compensated if the contract ends.

Beyond annual vacations, the Ghanaian framework contains clear safety nets for medical issues and family needs, mirroring the socio-cultural dynamics of the region:

Sick Leave: Employees are entitled to paid sick leave allocations when incapacitated by illness or injury, provided they present a validated medical certificate from a registered practitioner. The exact duration and payout structures vary by company policy or collective agreements, as the Labour Act leaves specific terms flexible provided the basic right to sick leave is respected.

Maternity Leave: Female professionals are heavily protected under Section 57, granting them at least 12 weeks (84 days) of fully paid maternity leave in addition to their annual leave entitlement. This baseline can be extended by an additional two weeks if there are complications during childbirth, during which full job security and salary benefits are legally maintained.

Continuous Service Completed

├── 1 Year of Service: 15 Working Days Minimum Paid Annual Leave

├── Maternity Trigger: 12 Weeks Minimum 100% Fully Paid Leave (Plus Annual Leave)

└── Termination Notice: Linked to tenure (Up to 1 Month or more for permanent staff)

When an employment relationship must be dissolved, offboarding must follow strict statutory notice windows—ranging from one week for short-term or probationary employees to one month or more for permanent, confirmed staff—or payment in lieu of notice. Unless serious misconduct (faute lourde) is explicitly proven through a formal disciplinary hearing, departing workers are entitled to all outstanding salary balances, accrued untaken leave pay, and contractually agreed severance.

Furthermore, if a separation occurs due to corporate restructuring or downsizing, it is legally classified as a redundancy, requiring a formal notification to the Chief Labour Officer and negotiations regarding redundancy pay (severance allowance). An Employer of Record (EOR) Solution in Ghana partner ensures that every step of this delicate termination lifecycle is handled perfectly, protecting your brand from painful wrongful termination disputes before the National Labour Commission (NLC).

7. Entity Incorporation vs. Agile Deployment: Why Forward-Thinking Brands Choose Employer of Record (EOR) Solution in Ghana

For international leadership defining their expansion playbooks for West Africa, the ultimate choice rests on a clear comparison: Is it better to incorporate a standalone local subsidiary, or should your enterprise leverage the immediate agility of an in-country Employer of Record? Registering a traditional legal entity in Ghana through the Registrar General’s Department (RGD) and the Ghana Investment Promotion Centre (GIPC) requires navigating a lengthy, multi-step process.

It demands significant minimum foreign capital requirements, local registration fees, processing individual tax registrations, physical bank account setup within local constraints, and hiring internal accounting and legal experts to process monthly GRA and SSNIT filings. This setup path routinely takes three to six months to complete, exposing your expansion strategy to market friction and fast-moving regional competitors.

Choosing to partner with a licensed Employer of Record (EOR) Solution in Ghana provider completely transforms this operational timeline. Because the Employer of Record (EOR) Solution in Ghana provider already operates a fully compliant, locally registered corporate entity in Accra, the entire onboarding and localized hiring sequence can be completed in as little as 48 hours.

The Employer of Record (EOR) Solution in Ghana partner absorbs all statutory employer liabilities, drafting bulletproof local contracts under Act 651, calculating complex overtime premiums, processing monthly SSNIT and progressive PAYE filings, and administering all mandatory annual and medical leaves. This rapid deployment model eliminates heavy upfront setup costs, allowing your leadership team to focus entirely on core business priorities like market validation, scaling operations, and driving client acquisition.

Furthermore, if your firm ever needs to adjust its regional strategy, an Employer of Record (EOR) Solution in Ghana framework allows you to wind down operations within standard notice guidelines, completely avoiding the lengthy, bureaucratic, and costly process of liquidating a local subsidiary.

8. Strategic Action Checklist for Corporate Risk Mitigation

To safeguard your organization’s cross-border expansion, executive leadership, legal counsel, and human resource heads should execute the following operational audit protocol:

[ ] Audit Remote Staff Classifications: Immediately review all active independent contractor agreements in Ghana. Evaluate whether these individuals are utilizing corporate equipment, working regular exclusive hours, or reporting to managers in a way that aligns with standard employment.

[ ] Recalibrate 2026 Compensation Projections: Update all financial models for senior staff to reflect the expanded GH¢ 69,000 monthly SSNIT cap and ensure the mandatory 13% employer contribution is properly budgeted.

[ ] Verify Working Hours & Overtime Policies: Ensure remote tracking software accurately records hours against the standard 40-hour workweek, protecting the firm against backdated overtime claims before the National Labour Commission.

[ ] Incorporate Local Specialized Reliefs: Work with your localized payroll partner to confirm that resident employees receive access to statutory reliefs (such as the personal, spouse, and child relief allowances) via the GRA portals.

[ ] Establish a Legal Entity Barrier: Migrate your distributed teams onto a certified local EOR structure to eliminate Permanent Establishment risk and insulate your international corporate revenue from local tax authority claims.

Securing Your Business Future in Ghana

The rapidly evolving economic landscape of Ghana presents an exceptional array of opportunities for companies eager to leverage the country’s strategic position and talented workforce. However, as the Ghanaian government tightens compliance checks through digital portals like the GRA e-services platform, there is no longer any room for administrative shortcuts or informal employment setups. Managing an international team across borders requires deep, specialized local compliance expertise.

By choosing to partner with a premier provider of Employer of Record (EOR) Solution in Ghana, you bridge the gap between global expansion goals and local legal mandates. An Employer of Record (EOR) Solution in Ghana provider allows your organization to hire top talent in Accra with confidence, maintain flawless alignment with the Ghana Labour Act, protect your business from permanent establishment exposures, and run an optimized payroll setup.

Share your experiences, operational questions, or expansion plans in the comments section below, or reach out to our dedicated professionals to arrange a detailed workforce compliance audit using Employer of Record (EOR) Solution in Ghana.

If you found this strategic compliance blueprint valuable, please share it across your professional networks to help other executives successfully navigate the landscape of global mobility.

Frequently Asked Questions (FAQs)

What are Employer of Record (EOR) Solution in Ghana and how do they manage corporate risk?

Employer of Record (EOR) Solution in Ghana act as a compliance mechanism where a licensed provider serves as the legal employer of your local staff. While your company directs day-to-day work, the Employer of Record (EOR) Solution in Ghana provider takes on all statutory liabilities under the Ghana Labour Act, 2003, handling local employment contracts, processing monthly payroll, and managing remittances to protect you from misclassification penalties.

What are the 2026 SSNIT contribution boundaries for employers utilizing Employer of Record (EOR) Solution in Ghana?

The maximum monthly insurable earnings ceiling is capped at GH¢ 69,000.00, meaning the top monthly Tier 1 contribution reaches GH¢ 9,315.00. Employers are legally required to contribute 13% of an employee’s basic salary, while the employee covers a 5.5% deduction, combining for an 18.5% total pension asset allocation split across approved tiers.

How are individual resident income taxes calculated under the current GRA PAYE framework?

Ghana utilizes a progressive personal income tax system ranging across seven distinct bands from 0% up to a top marginal tax rate of 35% for monthly chargeable income exceeding GH¢ 50,000. Non-resident individuals who provide services locally are subject to a flat 25% withholding tax at source without standard relief brackets.

What is the statutory notice period for terminating a confirmed contract under Act 651?

For short-term or probationary staff, notice is statutorily established at one week (seven days). For confirmed permanent personnel, the required written notice window scales up to one month or more, depending on the explicit terms of the contract and tenure guidelines. Terminations also require settling all outstanding accrued leave balances and any applicable redundancy packages to ensure compliance with the National Labour Commission.

Can an international business pay its Ghanaian employees in foreign currency like USD?

While compensation values can be contractually benchmarked against foreign currencies like the US Dollar (USD) to offer stability against inflation, the local payroll execution, monthly SSNIT reporting, and GRA PAYE tax remittances must be calculated and disbursed in Ghana Cedis (GHS) using approved central bank exchange valuations. Your provider of Employer of Record (EOR) Solution in Ghana handles this dual-currency processing automatically.

Employer of Record (EOR) vs. Professional Employer Organization (PEO) in Nigeria: When expanding your business into Africa’s largest economic ecosystem, navigating the choice between an Employer of Record (EOR) vs. Professional Employer Organization (PEO) in Nigeria is the most critical compliance decision your company will make.

The global scramble for top-tier African talent is no longer a future trend—it is a present-day reality. Driven by a massive, highly educated, tech-savvy, and English-speaking youth demographic, Nigeria has solidified its position as a primary hub for international recruitment. Global enterprises, fast-scaling technology startups, and international non-profits are racing to hire Nigerian software engineers, digital marketers, data analysts, and operations managers.

However, scaling a distributed team in Nigeria comes with a notorious hurdle: compliance.

Navigating foreign employment laws can feel like walking through a regulatory minefield. Nigeria’s regulatory framework has undergone massive shifts due to sweeping tax reforms, aggressive audits by state internal revenue boards, and landmark updates to local labor standards. If your company misclassifies a worker, bungles a local tax remittance, or fails to provide statutory benefits, you face severe financial penalties, operational shutdowns, and crippling lawsuits at the National Industrial Court.

To support a remote or localized workforce, international businesses generally weigh two primary paths: partnering with an EOR provider or utilizing a PEO. While these terms are frequently tossed around interchangeably by sales representatives, they represent fundamentally different legal, financial, and operational frameworks. Choosing the wrong model can set your expansion plans back by months and cost tens of thousands of dollars.

This comprehensive guide will break down the structural differences between an Employer of Record (EOR) vs. Professional Employer Organization (PEO) in Nigeria. Backed by the latest 2026 legal updates, this blueprint will help you determine the exact workforce strategy needed to scale your Nigerian team legally, safely, and efficiently.

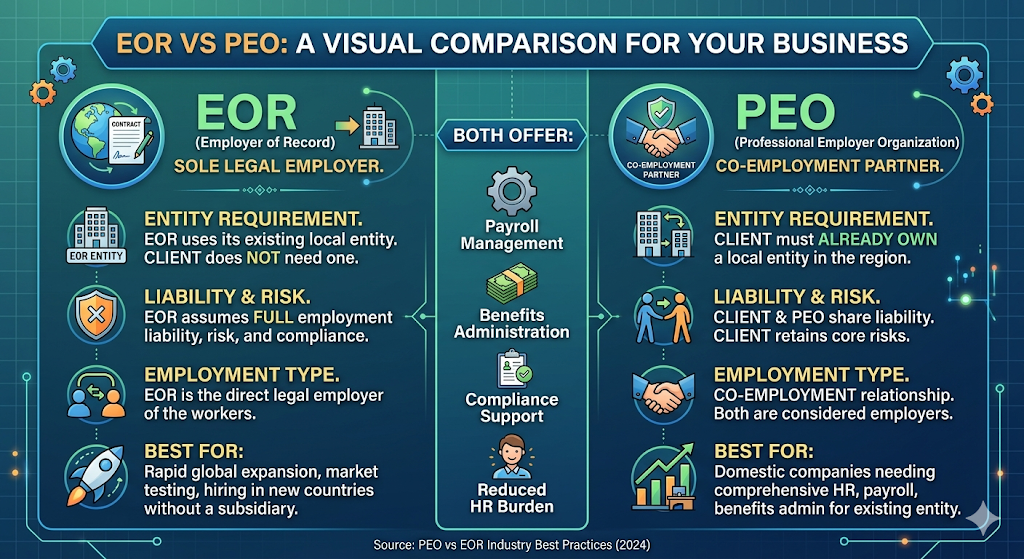

1. Defining the Core Structures: Employer of Record (EOR) vs. Professional Employer Organization (PEO) in Nigeria

To make an informed global expansion decision, you must first understand the core legal mechanics that separate these two employment architectures.

[EOR Model Architecture]Your Company <─── (Day-to-Day Operational Management) ───► Employee

│ ▲

▼ │

EOR Provider ◄──────────── (100% Sole Legal Employer) ───────────┘

[PEO Model Architecture]Your Company ◄─── (Co-Employment Liability Framework) ───► PEO Provider

│ │

└─────────── (Shared / Joint Legal Employers) ────────────┴──► Employee

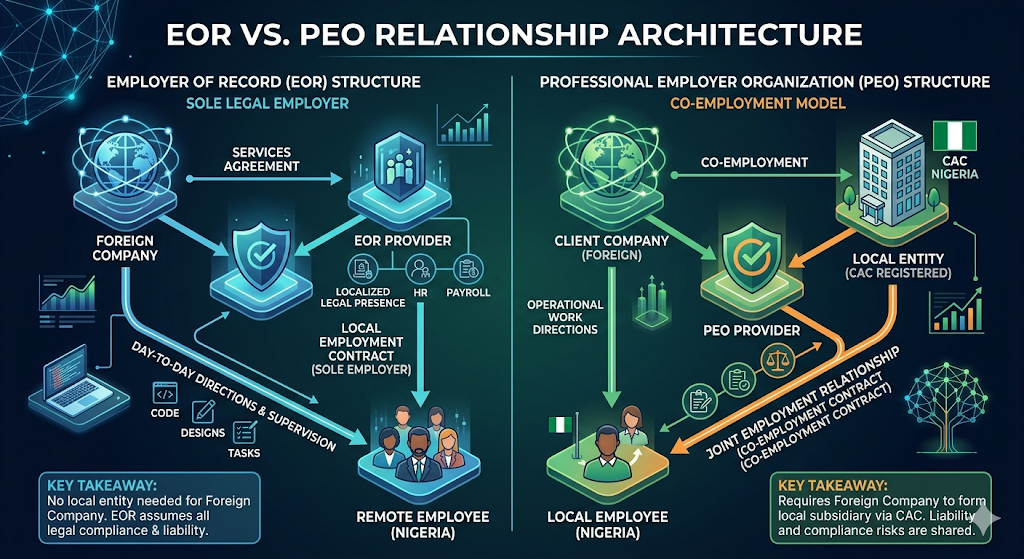

What is an Employer of Record (EOR) in Nigeria?

An Employer of Record (EOR) is a third-party organization that becomes the sole legal employer of your staff in Nigeria. Under this arrangement, the EOR provider assumes 100% of the employment liability, compliance risks, and administrative burdens.

The EOR hires the worker through a locally compliant employment contract that satisfies the strict mandates of the Labour Act (Cap L1, LFN 2004). They handle local onboarding, run monthly payroll in Nigerian Naira (NGN), calculate and withhold progressive Personal Income Tax (PIT), and remit all mandatory social security contributions to the appropriate government bureaus.

The beauty of the EOR model lies in its operational division: while the EOR serves as the legal employer on paper, your company retains 100% day-to-day operational control. You manage the employee’s tasks, workflows, performance reviews, and daily deliverables exactly as you would with any internal team member.

What is a Professional Employer Organization (PEO) in Nigeria?

A Professional Employer Organization (PEO) operates on a co-employment model. When you partner with a PEO, a joint legal relationship is established: your business and the PEO share the responsibilities and liabilities of employment.

The PEO acts as your administrative HR department, managing heavy-lifting tasks like payroll processing, benefits administration, and tax filings under its own corporate umbrella. However, because it is a co-employment structure, your company remains a legal employer of record.

This shared liability creates a distinct operational prerequisite: to utilize PEO services in Nigeria, your foreign business must already have an established, registered legal entity within the country. The PEO simply hooks into your existing local corporate infrastructure to streamline HR operations.

2. Bypassing Entity Registration: The Operational Reality of Employer of Record (EOR) vs. Professional Employer Organization (PEO) in Nigeria

The fundamental difference between these two systems shapes your initial expansion timeline, upfront capital expenditures, and corporate compliance strategy. It boils down to a simple question: Are you ready to establish a permanent corporate subsidiary in Nigeria?

The Reality of Setting Up a Nigerian Subsidiary

If you choose the PEO route, your expansion journey must begin at the Corporate Affairs Commission (CAC), the government body responsible for regulating the formation and management of companies in Nigeria.

Registering a foreign-owned subsidiary through the CAC is a resource-heavy, bureaucratic process. Under current regulations, it requires:

Substantial minimum share capital requirements (often set higher for foreign-owned enterprises).

Appointing local company directors and corporate secretaries.

Opening commercial local corporate bank accounts within Nigeria.

Registering with the Federal Inland Revenue Service (FIRS) and respective State Internal Revenue Services (such as the LIRS in Lagos).

This process typically takes between 2 to 4 months of bureaucratic processing and costs anywhere from $15,000 to $50,000 in legal fees, structural setup costs, and ongoing administrative overhead.

How an EOR Provides a Turn-Key Legal Short-Cut

For businesses looking to avoid entity setup, an EOR serves as an immediate alternative. Because the EOR provider has already heavily invested in building its own compliant corporate infrastructure, registered local entities, and expert HR teams within Nigeria, you bypass the CAC entirely.

By utilizing localized EOR frameworks, your international business can identify a target candidate, execute a master service agreement with the EOR provider, and have that employee legally onboarded and working within 1 to 2 weeks. This unlocks unparalleled speed-to-market, allowing startups and enterprises alike to test product-market fit or scale up remote engineering teams without long-term legal entanglements.

3. Comparing Legal Liabilities: Employer of Record (EOR) vs. Professional Employer Organization (PEO) in Nigeria

Understanding the risk allocation between an Employer of Record (EOR) vs. Professional Employer Organization (PEO) in Nigeria requires a deep dive into the regulatory enforcement landscape. The Nigerian government, via its state and federal tax authorities, has drastically stepped up compliance monitoring to maximize non-oil revenue collection.

1. The Dynamic Minimum Wage Landscape

Following the historic passage of the National Minimum Wage Act, the federal statutory minimum wage is benchmarked at ₦70,000 per month (gross) for full-time employment. However, compliance is highly regionalized.

As of 2026, dynamic regional adjustments have created a highly fragmented wage landscape across different states:

Lagos State: Has scaled its minimum wage baseline up to ₦85,000 per month.

Imo State: Leads the baseline chart with an approved minimum wage of ₦104,000 per month for public sectors, driving up private sector compensation expectations.

Rivers State: Disburses a baseline of ₦85,000 per month.

Employers must ensure that an employee’s fixed basic pay meets these hyper-localized thresholds. Variable performance bonuses, one-off allowances, or benefits-in-kind cannot be used to artificially “fill the gap” to hit the statutory floor.

2. The Progressive PAYE Tax Bracket Redesign

The tax framework utilizes restructurings for the Pay-As-You-Earn (PAYE) Personal Income Tax (PIT) brackets. Payroll systems must apply these progressive bands after factoring in updated Consolidated Relief Allowances (CRA):

Annual Taxable Income Band (NGN)

Tax Rate (%)

First ₦800,000 or less

0% (Full Tax-Free Threshold Exemption)

₦800,000.01 to ₦3,000,000

15%

₦3,000,000.01 to ₦12,000,000

18%

₦12,000,000.01 to ₦25,000,000

21%

Above ₦25,000,000

24%

3. Progressive Rent and Accommodation Reliefs

Rent Relief: Workers can claim a specialized tax exemption of 20% on their annual rent payments, capped at a maximum deduction of ₦500,000 per year, subject to proper state filing and declaration.

Accommodation Benefit-in-Kind (BIK): When an employer provides housing benefits, the taxable benefit value is strictly capped at a maximum of 20% of the employee’s annual gross employment income.

4. High-Value Severance Tax Exemptions

To shield transitioning workers, compensation for loss of employment (severance pay) is granted a tax-exempt status up to ₦50 million. Any severance amount paid beyond this ₦50 million ceiling is pulled into the progressive PAYE tax net.

5. Increased Judicial Enforcement

The National Industrial Court of Nigeria (NICN) has drastically increased its scrutiny of worker exploitation, improper termination, and employee misclassification. If an international business treats a local worker as an independent contractor when their daily operations mirror a full-time employment relationship, the NICN heavily penalizes the firm, forcing back-payments of taxes, pensions, and statutory benefits.

The Liability Risk Factor: Under an EOR model, if a payroll settings toggle is misconfigured or a tax deadline is missed, the EOR provider suffers the penalties and legal heat. Under a PEO co-employment model, your business shares that legal liability, exposing your CAC-registered entity directly to the FIRS, state tax boards, and the National Industrial Court.

4. Statutory Payroll Compliance and Financial Math in Nigeria

Executing a compliant payroll process via a global payroll provider Nigeria requires managing separate payments to multiple distinct government bodies. For foreign companies, calculating these gross-to-net deductions accurately each month is an operational headache.

Whether managed entirely by an EOR or co-managed with a PEO, your workforce strategy must seamlessly account for these core statutory deductions:

The Pension Reform Act 2014

For any employer with 15 or more staff members, enrollment in the national pension scheme is strictly mandatory. The contributions are calculated as a percentage of the employee’s monthly emoluments (which includes basic salary, housing, and transport allowances):

Employer Contribution: 10%

Employee Deduction: 8%

Total Pension Flow: 18% remitted to the employee’s chosen Pension Fund Administrator (PFA) within 7 days of salary payment.

Group Life Insurance: Under this same act, employers must fund a comprehensive group life insurance policy valued at a minimum of three times the employee’s total annual compensation.

National Health Insurance Authority (NHIA) Act

For organizations employing 10 or more individuals, healthcare coverage is a statutory requirement.

Employer Contribution: 10% of basic salary.

Employee Deduction: 5% of basic salary.

Coverage: This mandatory scheme covers primary medical care for the employee, their spouse, and up to four dependent children under the age of 18 through accredited Health Maintenance Organisations (HMOs).

Nigeria Social Insurance Trust Fund (NSITF)

Administered under the Employee Compensation Act, this is an employer-only contribution of 1% of total monthly payroll. It funds a centralized national safety net that provides financial compensation and rehabilitation for workers who suffer work-related injuries, occupational diseases, disabilities, or workplace fatalities.

Industrial Training Fund (ITF)

If your corporate operations scale to employ 5 or more workers, or if your local entity achieves an annual turnover of ₦50 million or more, you must contribute 1% of your entire annual payroll to the ITF to fund national vocational and technical training initiatives.

National Housing Fund (NHF)

Employees earning above the baseline must contribute 2.5% of their basic monthly salary to the Federal Mortgage Bank of Nigeria, which provides affordable housing loan access to Nigerian nationals.

[Gross Monthly Salary Components]

│

├──► Deduct PAYE Tax (0% - 24% Progressive Band)

├──► Deduct Employee Pension (8% of Emoluments)

├──► Deduct Employee NHIA Health (5% of Basic)

├──► Deduct Employee NHF (2.5% of Basic)

│

├──► Add Employer Pension (10% of Emoluments)

├──► Add Employer NHIA Health (10% of Basic)

├──► Add Employer NSITF (1% of Payroll)

└──► Add Employer ITF (1% of Annual Payroll)

│

[Net Pay Disbursed in NGN to Local Bank Account]

The Compliance Penalty Trap

Failing to track these dates and amounts triggers immediate financial penalties. For instance:

Pension Defaults: Attracts a 2% monthly interest penalty on all unremitted amounts.

NSITF Violations: Carries a baseline 10% penalty fee.

PAYE Delays: Missing the 10th-of-the-month deadline can lead to audit penalties and potential criminal prosecution for tax evasion.

An EOR functions as a corporate firebreak. They track these calendars, execute precise gross-to-net calculations, and handle the localized filings, keeping your organization out of harm’s way.

5. Intellectual Property and Data Privacy (NDPA) Under Both Models

For fast-growing technology companies, international product teams, and creative agencies, expanding into a foreign territory poses two massive risks: Intellectual Property (IP) leakage and data privacy breaches.

The IP Trap in Cross-Border Hiring

Under standard Nigerian common law and the Labour Act, IP created by an independent contractor or an improperly structured employment layer can easily become legally ambiguous. If an employee creates proprietary software code or design while working for a foreign firm that lacks a local legal entity, claiming absolute ownership during subsequent venture capital audits or M&A due diligence can trigger legal gridlocks.

How an EOR Solves This: Premium EOR providers use master corporate services agreements coupled with localized tripartite employment contracts. These agreements explicitly contain ironclad, automatic IP assignment clauses recognized under Nigerian law. The moment your developer writes a line of code, the IP is legally transferred from the employee to the EOR, and automatically assigned directly to your parent enterprise.

The PEO Approach: Since a PEO operates under a co-employment framework, they generally leave corporate IP protection strategies entirely up to you. Your legal team must independently draft and execute supplementary Non-Disclosure Agreements (NDAs) and IP assignment contracts to protect your core business assets.

Data Privacy under NDPA

The regulatory landscape is heavily policed by the Nigeria Data Protection Act (NDPA). Any entity processing the personal data of Nigerian citizens must implement strict data privacy controls.

An EOR manages full compliance with data protection policies during onboarding, payroll, and benefits processing. This ensures your organization avoids the severe financial fines levied by the Nigeria Data Protection Commission (NDPC) for data mishandling.

6. Strategic Comparison Table: Employer of Record (EOR) vs. Professional Employer Organization (PEO) in Nigeria

To give your executive leadership team full clarity, let’s look at a head-to-head operational comparison of how these services function side-by-side in the Nigerian market.

Feature / Aspect

Employer of Record (EOR)

Professional Employer Organization (PEO)

Local Entity Requirement

Not Required. You utilize the EOR’s established legal entities.

Mandatory. You must register a local subsidiary with the CAC.

Employment Structure

Sole Legal Employer. The EOR assumes 100% employer status.

Co-Employment. Shared legal relationship between you and the PEO.

Compliance & Legal Risk

Transferred entirely to the EOR provider.

Shared Risk. Your entity is exposed to local legal disputes.

Onboarding Speed

Extremely Fast (1 to 2 weeks).

Slow (2 to 4 months due to entity setup timelines).

Cost Structure

Predictable flat monthly fee per employee ($300 – $600).

Typically a percentage of gross payroll (2% to 12%).

Intellectual Property (IP)

Automated, ironclad IP assignment built into local contracts.

Left up to your company’s independent legal frameworks to secure.

Best Suited For

Testing markets, remote teams, rapid scaling, and small cohorts (1-20 staff).

Long-term market permanence with large local workforces (50+ staff).

7. The Final Verdict: Choosing Between an Employer of Record (EOR) vs. Professional Employer Organization (PEO) in Nigeria

To choose between an Employer of Record (EOR) vs. Professional Employer Organization (PEO) in Nigeria for your international workforce expansion, evaluate your long-term operational goals against this clear decision matrix:

Scenario A: The Agile Tech Startup or Mid-Market Firm Testing the Waters

Your Goal: You want to hire 2 software engineers and 1 product manager in Lagos immediately. You are unsure of what your long-term African corporate presence will look like over the next 24 months.